From time to time, I like to provide updates on my own personal finances and my investment strategy. You may recall that I’ve been invested with Lending Club, for a little over 2 years now. It’s certainly had it’s up and downs (early scare with a couple of bad loans then some good notes paying consistently) and has been a good experience. Although initially I recommended it, I’m backing down on my recommendation. It’s still a cool concept that I think could be an interesting investment opportunity, but I think that for most young professionals, I wouldn’t recommend it as an investment.

A reminder of what it is

You can go back and read my past articles, but in a nutshell, Lending Club matches people that have some money to lend (investors) and people that need to borrow money (borrowers). It’s often a good match as borrowers can get a lower interest rate compared to what they might get elsewhere in the market and investors can get a higher interest rate from putting their money in a savings account or other investments. Notes are issues in $25 increments (i.e. you can borrow several thousands but you’d only lend $25 to a single borrower thus diversifying the risk if the borrower defaulted) and are borrowed for either 36 or 60 months. Loans are paid back over that period. There’s always a risk that a borrower might not pay back, and the loans are not secured (i.e. the borrower doesn’t have to put down any collateral).

My results so far

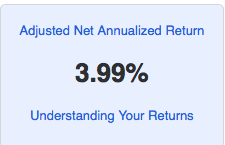

Over the past year, I’ve had an investment return as high as 10%, but now it’s fallen to 3.99% annualized return. 4% is certainly better than 1% I’m getting with my online savings account, but much less than some of the index funds that I’m invested in. I’ve had 4 notes that have been charges off, and although I haven’t lost all $25 of my money, I’ve lost about $15/note. I’ve had a couple pay off early, and then most of the others falling in the “current” category.

I’ve consistently been focused on notes that are being used for “loan consolidation” or “debt refinancing” loans. I feel like those borrowers are going to be more motivated and likely to pay off their loans. These are borrowers that are likely in debt with high interest credit cards, and Lending Club offers them a chance to pay down that debt at a lower interest rate. I stay away from “business” or “vacation” or “other” notes as I think those are probably a bit riskier.

Where I think it went wrong

Although I enjoyed some early success with most of my notes paying off, I don’t think I had enough money invested to better pad the poor performing notes with the good performing notes. I only had $500 invested, which was starting with 20 notes. Of those 20, I don’t think I had enough to diversify my holdings so when a couple got charged off, it really hurt my overall return. I think if I had invested more (which I wasn’t comfortable with), I may have had better success.

My plan moving forward

I’m not able to pull out all my money right now, as much of it is lent out in the form of notes. I’m not putting more money in (as I had been doing from time to time) and will be slowly pulling money out over time. I’m still investing in a few new notes (the $.75 or so each note pays add up to $25 and I’ll invest in another note), but not as many as I much was.

Overall Lending Club was certainly a fun experiment to review and check out. Early on results were promising (a 10% return is pretty sweet!) but over time it’s fallen and I can put my money in better places. A 4% return just isn’t worth the risk that I’m taking with these notes.

Although Lending Club isn’t necessarily a bad place to invest your money, I think that young professionals can put their money in other better alternatives (like index funds).

I put $2500 in and only got a 1% return (yes it started around 10%). I’m not reinvesting, and each month I’m able to pull out about $100. Lending club is better for big investors that want to put 100s of 1000s of dollars.

Great article Ben — I like how you are willing to retract a previous statement — it shows that you are dedicated to your readers.

Cheers!

Dave